Creating havoc since 2006. Fair use is claimed for images on this site, but they will be removed (if owned) on request out of politeness. movingnorth@gmail.com

“I am altering the deal. Pray I don’t alter it any further.” – The Empire Strikes Back

Am I the only one still trying to forget Game of Thrones?

Today, we’re diving into silver like Scrooge McDuck® into his money vault, mainly because I think it tells a much deeper story about wealth and reality. Silver prices have doubled since April. More than that, really. But who’s counting?

What’s causing this?

First, the dollar is worth less. Not worthless, though I think anyone checking in from the time the Fed® started back in 1913 would disagree. No, that delightful dumpster fire comes later, probably around the time Tim Walz starts quoting Marx in his next speech.

But worth less? Absolutely. Inflation is like a bottle of Everclear® showing up at a high school kegger. You know it shouldn’t be there, but everyone is enjoying the party so much that no one wants to pour out the booze. And, no one has poured out the booze. People just keep showing up with more and more booze. And by booze, I mean printing money.

Everclear© eventually turns brains into goo, and the Fed® is turning our money into an unsightly goo. That’s okay, because who needs actual value when you can just ctrl+p your way to prosperity?

Silver’s price jump isn’t because silver suddenly got sexier; it’s because greenbacks are now less than a dime a dozen. Okay, not a dime a dozen, but a silver dime is from 1960 is worth $7.87 at $110 an ounce silver.

I have a dime in one hand and a nickel in the other. What am I? Broke.

I know, I know, there is nothing new here. Rome. Weimar Germany. Zimbabwe. Venezuela. History’s a harsh teacher, and not one of the hot ones that just graduated from college that was a hot blonde with long hair that drove a Trans-Am® while I hummed Hot For Teacher in the back row of the classroom in 11th grade English.

Sorry, that was oddly specific.

Second, a driver of this rise in silver prices is A.I. A.I. is in everything now, including French’s® Classic Yellow Mustard™, at least according to the label. But silver is in computer chips, solar panel, and chemical catalysts. Industry actually consumes the stuff at a rate of 680 million ounces per year. Yes, that’s a lot, being a bit more than an Ohio-class ballistic missile submarine or the weight of cash exported by Somalians from Minnesota each week.

Everything’s fine, though, right? We’ve been doing this forever.

Not so fast, Pat Sajak. The dragon has entered the chat. No, not George R.R. Martin. He’s the walrus. By dragon, I mean:

China.

Dragons don’t explode, but a dino might.

They’re the primary refiner of silver according to some sources, though I’ve been unable to back that up with a source I really trust, so take that as a “trust me, bro” type of number. Recently, though, China looked around and they do control about 15% of silver production and third of the industrial supply goes through China.

On January 1, China changed its rules. It will only license exports to specific companies for specific uses. No more “hey, buddy, can I get a pallet of silver for my Etsy® jewelry shop?”

Nope.

Remember that old Lenin quote where he said that the capitalists would sell the commies the rope to hang the capitalists?

We’re living it.

We outsourced everything except Learing Centers to China because China did it cheaper: rare earth mining and refining, silver mining, manufacturing, bad fashion choices. You name it.

“Why get all sweaty and dirty when we can push paper instead?” was the attitude. So, we traded factories for finance, blue collars for spreadsheets. Now, the know-how’s gone east, poof, like a magician’s rabbit.

Entire industries vanished from the U.S.

Health is wealth. Don’t believe me? Check out the prices of fresh kidneys! (meme as found)

This is the bill coming due for all that cheap Walmart® crap from China. We’re paying premium now, and it won’t just be in dollars it will be in our international standing and living standard.

Third: it’s the paper. Silver’s price used to be all about paper: silver futures, silver options, the whole Wall Street silver casino. Sweaty guys in New York could bet on silver in Hong Kong without ever touching it. It’d never come within 5,000 miles of their Manhattan condo.

It was like playing poker at a casino where people kept trading IOUs. Nobody cashed out their IOUs for the real chips. The market was dominated by speculators, hedge funds, a particular big bank, and day traders who treated it like a video game.

This was profits without product. But oh, how the tables have turned.

Now, the game’s gone real-world, and folks are demanding delivery. Warehouses are being sacked like a Domino’s Pizza® after Weedfest© in Colorado. Empty shelves, frantic calls, bummed out hippies, the works.

(as found)

Take Samsung©, for instance. Reports say they hopped on a plane, jetted to Mexico, and straight-up bought out the silver supply from at least two mines for the next few years. No matter what it costs, they’ll buy it all, plus front the company the cash to get capacity up to snuff. That’s not hyperbole; that’s desperation with a corporate jet.

Why? Because silver’s a tiny part of their widgets: phones, TVs, fridges. But it’s an essential part of their widgets. The recipe calls for it, like flour in a cake. Skip it, and the chip in the phone won’t work. Redesigning? Yeah, maybe. That takes time, money, and R&D. The engineers would be pulling all-nighters, and all of a sudden the coffee market is impacted.

It’s far easier to pay $100 or even $200 an ounce. Even at $200, it’s just a buck or two per gadget. Compare that to shutting down production lines, which would be a corporate catastrophe. They’re going to buy the silver. Sure, there’s a breakeven, and it will vary by use: I saw one as low as $134. Less silver jewelry will be made. Werewolves will go unhunted.

Finally, the biggest risk for most people reading this is that it shines a spotlight on the made-up money system for what it is: made-up promises, ink on a ledger or magnetic bits on a hard drive. Silver, gold, copper, lead, corn, PEZ®, that’s real. It’s tangible, you-can-hold-it-in-your-grubby-paws stuff and eat it our swim in it if you’re Scrooge McDuck©. Fiat currency? It’s money conjured out of a belief system, a collective hallucination we’ve all bought into since LBJ printed bucks for Vietnam and Nixon got called on our “gold-backed” bluff by the French.

Hmmm, which one? (as found)

The dollar has been floating on faith ever since, like Wile E. Coyote™ before he looks down. But now, with silver spiking, the fall is in sight. People want assets, not abstractions. It’s the ultimate vote of no confidence in the dollar downsizing derby.

Is silver in a bubble?

Beats me. Maybe.

Maybe not.

Is the dollar in an anti-bubble and collapsing first in slow motion and then all at once?

Beats me. Maybe.

Maybe not.

Silver could crash tomorrow or double by next month. But my gut says $20 or even $50 silver is in the rear-view mirror, except for after a deflationary collapse temporarily crushes it. I think it has vanished like cops without tattoo sleeves or the McDonald’s® Dollar Menu™ where something on the menu actually cost a dollar.

It’s just gone.

I’m sure it’ll be fine.

But, hey, what are you worried about? Chuck just showed up with more Everclear®! Party on!

Disclaimer: I write funny things, and you should know that by now so this isn’t investment advice or fashion advice or love-life advice. Think for yourself and do your own research and stop copying me! Teacher, he’s copying me!

Disclosure: I do have a position in silver that I’ve had forever, and bought (literally) about a hundred and thirty bucks more today in my IRA, which might have been stupid, but, whatever. If you think this article will move the international silver price, you’re stoned.

“Get someone else to run your scams.” – The Shawshank Redemption

My brother wanted to play cowboys and Indians. I got out my six gun cap pistol and he bought a motel. (all memes except the Motel 6® meme are as-found)

Let’s talk about India.

Again.

Over decades, Indian immigrants (legal and illegal) have created a real-life version of Invasion of the Body Snatchers, but instead of pods, it’s Patels. And Singhs. If capitalism is a game, Indians are using cheat codes, and nobody’s hitting the reset button because, Heaven forbid, someone calls foul and gets labeled a bigot.

Let’s start with the motel mafia, aka the Patel Hotel-Motel Cartel. Back in the 1940s and ’50s, Indians from Gujarati (I think that’s how someone with dyslexia spells guitar) kicked things off in California, leasing rundown single-room occupancy joints in California. Back then, only 100 Indians (total) a year were allowed into the United States. Now, I think that’s the minimum amount of Indians that enter a Costco® within 10 minutes after it opens each morning.

Thanks to the 1965 Hart-Cellar Act, starting in the 1960s, the Patels could begin to chain-migrate everyone back in the village, and boy did they ever.

During the 1970s inflation crisis, American motel owners had to dump properties like bad dates because people couldn’t afford to travel. Kind of like fast food today, eh?

If I fell for a tech support scam, am I and Indian giver?

Enter the Patels. They snapped up distressed motels for peanuts, often with family loans, because banks and insurers wouldn’t loan them cash because, you know, scammers. According to Mythosnoir’s Substack® (LINK), at a fire marshal convention one year, they claimed that Patels set fire to their motels and submitted phony claims. It’s a long read, but interesting.

I’ve seen one Patel submit a phone claim (and this in 2022) so I’m pretty sure it’s not an exaggeration. Their response was to form their own insurance company.

But how does the scam work? One Patel buys a motel, brings brothers, cousins, uncles, and the village goat-herder in. They work for below market wages and live in the crappiest rooms in the hotel because it’s all in the family, and everyone’s dreaming of their own Patel Motel and no one is paying income tax because why would you report it like a rules-following rube?

Then, the first Patel sells to another Patel at a markup, rinse and repeat.

It’s a closed loop: be a Patel, buy from a Patel, hire Patels, get loans only for Patels from a bank owned by . . . a Patel. Oh, and often with Small Business Administration, you know, .gov, funding.

Today? Gujaratis own over 60% of U.S. hotels, and Patels snag 80-90% of motels in small towns.

Be very afraid.

Mythosnoir also indicates that, if Indians got 50% of the hotel SBA loans, that’s $7.5 billion fronted backed by you and me.

That’s not capitalism; that’s a clan economy plopped into America’s free market like a Bollywood dance number. And I said that the Patels own the banks. They do. Enter the “State Bank of Texas®”, was founded in 1987 by Chan Patel (of the Mumbai Patels).

Chan’s kids Sushil and Rajan (fine American names, those) in top spots. Want to make a bet on the ethnic composition of the bank? I tried to check, but their web presence was a website that looks like someone based on an old Geocities® fan page for Gillian Anderson filled with 404 links. It was designed in 2015-2018 and I checked half a dozen of their listed locations, and none of them were still owned by them.

Odd.

I had to.

And the other odd thing is that these Patel Motels around here never seem to have many guests. I’m not accusing, but hotels have seen fraud cases, from tax evasion to flipping schemes netting millions to money laundering. It would be nothing for human traffickers or actual drug cartels to meet up with motel Patels.

Zoom in to Augst, 2025 when ICE and the FBI arrested five Indians.

The crimes? Allegedly:

Allegedly. Over half a million in cash and “illicit drugs” whatever those are, were also reported as seized. The Patel hotel flipping scams? I didn’t make it up. Feds nailed Indians for $35 million in fake SBA loans for hotels (link below).

Three Indian-Americans indicted in over $35 mn loan fraud scheme

What a model minority!

The same sort of thing happens in trucking. Sikhs, mostly Punjabis, and seemingly all named Singh (as in every Singh-al time) control about 20% of the U.S. industry nationwide, and up to 40% on the West Coast. The crimes tied to them is milder, just vehicular homicides, drug trafficking (I mean, it was on 309 pounds of cocaine, just a dab), meth trafficking, organized cargo theft rings, etc.

Yup, a model minority through and through.

Like Patels, it’s chain migration: one gets a CDL, brings his family, they drive for low pay to “pay dues,” then start fleets. It’s just one Singh after another.

So, like the Patel bank, they loan only to themselves, and probably pay no taxes on the interest. I mean, they’re great credit risks as drivers, with CDLs obtained through cheating and little to no English. Why would you need to know how to safely drive a truck or read road signs to carry 80,000 pounds down the road at 80 miles per hour (Guptas per Gigawatt)?

Shortage or not, unqualified drivers kill.

These aren’t isolated incidents. It’s a broad pattern. Immigrants form closed societies, exploit high-trust laws like SBA loans and chain migration, undercut natives with cheap in-group labor, and capture markets because they’re not paying taxes. No diversity hires for them: it’s all clan.

Capitalism? Nah, this skirts antitrust, labor laws, tax laws and immigration rules.

Enforcement? Zilch. Call it out, and you’re “racist.” Meanwhile, American workers get squeezed. These economic empires siphon wealth into ethnic enclaves, not the broader economy. High-trust societies like ours assume people are going to engage in fair play, but low-trust immigrants will do anything to game the system.

I am glad I only made one joke about body snatchers. I didn’t want to get carried away.

“We, the soldiers of The National Liberation Front of America, in the name of the workers and all the oppressed of this imperialist country, have struck a fatal blow to the fascist police state.” – Escape from New York

I don’t watch soccer. If I wanted to see grown men try to score for 90 minutes, I’d go to a bar. (all tweets® as-found)

I’ve been to New York City once. I flew in to JFK, met with some friends, drove up north to a cabin he owned, and, drank some beer, and then saved the President from the Duke of New York (He’s A Number 1!) after his escape pod landed there.

That was fun. I mean, not the New York City part, but the beer and saving the President part. When I got to my friend’s apartment, it was a third-story Manhattan thing that was smaller than a closet. Yet, he was married, and two people lived in this tiny place.

It’s not like he was poor, either. He did okay, and his wife was an executive vice president at a company you’ve heard of.

They owned a car, and we were going to take it to their cabin.

How do you make a sandwich in Venezuela? Put a meat coupon between two bread coupons.

He asked me if I wanted to go with him to get it. What he meant was that he was going to take a taxi two miles to the building where it was stored. He had to schedule picking it up, because they packed the cars in like sardines and have to work a dozen our so out to get to his, which, after seeing it, probably took 20 minutes.

These were people that were in the 1%, and my life was easier in almost all respects even though I made a fraction of the money that they made.

I didn’t see the attraction of New York City then, and I don’t see it now. I mean, here in Modern Mayberry if I shoot my .30-06 off the back deck it’s Wednesday. But in New York City, it’s national news. But as bad as it in the Big Apple, it’s now worse.

Zohran Mamdani (by his name, a fine Irish lad, no doubt) was just elected Mayor. He’s not a Democrat. No, that’s not retarded enough. He’s a Democratic Socialist®. That must be like “extra-fancy” ketchup.

Mamdani’s policies are just as American as his name and upbringing. I mean, you can feel the love, because his Director of Appointments, Catherine Almonte Da Costa said back in 2016 posted, “It’s important that white people feel defeated.”

Whelp.

This was the woman hand-picking key officials in City Hall, and her worldview sees white folks as the enemy to be crushed. And Ms. Almonte Da Costa wasn’t alone. On Mamdani’s campaign trail, he called for raising taxes specifically on “whiter neighborhoods” to fund his socialist schemes.

So, it’s about money. And power. I mean, it always is, but most of the time they’re not so blatant. Let’s dig into his housing policies, for one. These seem designed to eviscerate the concept of private property altogether. On purpose.

Cea Weaver (her parents couldn’t afford a consonant for her first name) is Mamdani’s pick for Director of the Mayor’s “Office to Protect Tenants”. Weaver isn’t just a tenant advocate. Nope. She’s a full-throated opponent of homeownership itself. In her own words, she’s called for seizing private property and described individual homeownership as a tool of “white supremacy.”

Must be news to COMMUNIST China, which now has, what, a 90%+ homeownership rate? Re-read that. NYC is officially farther left than the CCP. Achievement unlocked!

Cea (I wonder if anyone besides me refers to her as the Cea-word?) believes homes should be owned collectively, like some throwback to the Soviet Union where the state decides who gets what (and who is: never you and what is: never what you want).

According to the NY Post®, Cea-word’s mom has a $1.6 million house in Tennessee.

Weaver’s background as executive director of Housing Justice for All® screams daddy issue GloboLeftist. What were those commies at Housing Justice for All in favor of?

Rent freezes, eviction moratoriums, and government takeovers that have already tanked property values in every progressive stronghold where they’ve been tried.

But it gets worse. I mean, worse than being in New York in the first place.

Mamdani’s support for the Community Opportunity to Purchase Act (COPA) is a dagger to the heart of property rights. Under this new law, if you want to sell your multifamily building, you must first offer it to the city and favored nonprofits. Like the Quality Learing Center. For how long? Six months.

Six months.

An owner must notify the Department of Housing Preservation and Development (HPD), and these friends of Zohan “qualified entities” get first dibs. If you finally get an offer from a private buyer, NYC and its pet nonprofits still have a right of first refusal to match the offer within 15 days.

But this is no surprise, since Mamdani has openly hailed South Africa as the blueprint for New York City. In his inauguration speech, he electrified his crowd by declaring, “South Africa is the model for New York,” praising its post-apartheid “transformative justice.”

South Africa now has more racial laws than it did under Apartheid. But the quality of life is better. Wait, what?

Have you heard about what’s happening in Johannesburg lately? That “model” is a crumbling mess of blackouts, rampant violence, street piracy, skyrocketing rape rates, and economic disrepair. South Africa is built on corruption scandals, farm seizures, and a GDP that’s flatlined

Great role model, but no coincidence. Mamdani’s family ties run deep into anti-Western activism. His father, Mahmood Mamdani, has long peddled narratives glorifying “resistance” movements, including defending suicide bombers. Apparently, the manual for suicide bombers is called C4 Yourself, but I digress.

The warm embrace of collectivism has resulted in the greatest tragedy in human history: communism in the twentieth century. That doesn’t matter. My guess? Lots of New Yorkers are going to be doing a real-life reenactment of Escape from New York.

Snake Plissken had it easy. He only had to escape roving bands of violent criminals who wanted to kill him. New Yorkers in 2026 will have to escape taxes, too.

“Don’t you know we in a war here?” – Forrest Gump

War isn’t always about who is right, but it always is about who is left.

Volume VII, Issue 8

Most memes except for the clock and graphs are “as found”. I have maintained the Clock O’Doom at 9., given the open support of assassination and criminality by the GloboLeft and the increase in violence as well as direct interference with ICE and the insertion of the military into law enforcement. Beware: the number can climb quickly.

My advice remains. Avoid crowds. Get out of cities. Now. A year too soon is better than one day too late.

In this issue: Front Matter – Stochastic Warfare – Misery Index – Updated Civil War 2.0 Index – Links

Front Matter

Welcome to the latest issue of the Civil War II Weather Report. These posts are different than the other posts at Wilder Wealthy and Wise and consist of smaller segments covering multiple topics around the single focus of Civil War 2.0, on the first or second Monday of every month. I’ve created a page (LINK) for links to all of the past issues. Also, subscribe because you’ll join nearly 840 other people and get every single Wilder post delivered to your inbox, M-W-F at or before 7:30AM Eastern, free of charge.

Stochastic Warfare

The Tweet® really does outline what many readers have been saying, namely, that we are under attack. Is it open warfare? Not exactly. It’s 5th or 6th generation warfare, fought on a civilizational scale on the timeline of generations. Against you.

And the person being attacked is . . . you. You don’t have to die now. First, they’ll encourage feminism and promote the idea of female empowerment meaning, “hey, let’s whore ourselves out during our twenties so we can’t pair-bond with men in our most fertile years” to create an environment where there is a “shortage” of people.

Again, this is not a company. It’s a country. A business can have a shortage of workers, a country can’t have a shortage of its own citizens. That’s nonsensical. It’s like saying my family has a shortage of members, so I’ll bring in an Indian. See? Nonsense. A country is much closer to a family than a company. If there’s a shortage of workers, the answer is to do things that increase native childbirth.

That’s it. If they liked you. Instead they work white men and women to pay for people who hate them.

This is how Stochastic War works.

No, their next step is to import millions of people that support the ideology of the progressive state, of globalism, of communalism. When these people arrive, inject them with the idea that they deserve the country. Now, since they don’t want to be American, and since they would fight against America if (say) America entered a war against Somalia or India they’re not committed to America. They’re just here to extract economic resources.

Once these people are imported, what then? They take your money. Your world is made poorer as the grift/scam/cash grab continues and recycles that money to foreigners and to GloboLeftist politicians. If you look at the graph below, you see that race plays a part in the way people vote and in who the Democrats want to import to retain power. Why do they want a lot of Indians (Gujarati)? Because they vote for the warmth of collectivism because more government systems mean more scams and corruption. Also, they have never had to deal with the Berlin Wall, which was built to contain the warmth of collectivism behind concrete and barbed wire, as collectivism always ends up.

This is how Stochastic War works.

There are ramifications of this war against you. If you didn’t hear, a black man stabbed a white guy. The white guy then said the evil gamer-word after being stabbed. This is not an unreasonable reaction, and is a far lesser offense than stabbing someone. The jury acquitted the black man, despite clear video of the attack.

This is Stochastic Warfare. Blacks learn that they can stab with impunity.

Black jurors, though, aren’t a jury of “peers” since statistically, they have been proven to be biased in favor of blacks. This destroys the justice system: it’s supposed to be blind, and your skin color or wealth or age or sex shouldn’t matter. We’re human, though, and rich guys can buy great lawyers, so the system has always had a skew to it. But without a functioning justice system, or worse, a justice system skewed to convict white people for crimes that are far beyond the offense (Derek Chauvin for murder) vigilantism will return.

Not might. Will.

Even when people are found not guilty, it costs hundreds of thousands of dollars to defend a murder case, and Daniel Penny rightly walked free, but what’s the cost?

This is how Stochastic War works.

This bias applies everywhere and you can see that black people hate white people, a lot, in Great Britian.

And The Washington Times story, below, is behind a paywall, but the headline speaks for itself:

The problem of a multicultural society isn’t limited to blacks. Other racial/ethnic groups like themselves best. Hispanics like Hispanics most. Blacks like blacks most. Asians like Asians most. But whites? They like everyone the same. That egalitarianism is crucial to making a multicultural society work, but multicultural societies never work.

And Great Britain now realizes this. Would they ask their moslem or Indian invaders to fight for them? Of course not, because they know that the moslems want to conquer the English rather than Crimea. The Indians? The Indians mostly are there for a buck and would run away back to Mumbai if they felt even slightly threatened. That leaves the white guys. Who will, once again, be faced with disproportionate death and injury.

Which is how Stochastic War works.

The mayor of London, who isn’t British, wants to make white people disappear. Literally:

And, you have people like this. This is in America.

It’s time to push back. It appears that the rapes and killings and theft have been enough and the Irish are pushing back against Stochastic War.

I think that @dystopiangf is right. We are in the midst of a quiet, Stochastic War that has been going on for decades, almost certainly since before I was born. What we are sensing right now is the time when people realize, and finally accept that this Forgotten War (I wrote a song about this LINK, you should listen to it because it’s pretty badass) against cultures we vanquished centuries or thousands of years ago is going on.

As people awaken, we’ll see what people have always seen as demographic changes occur: open war. Remigration is the kindest choice, but here we are.

Buckle up.

Misery Index

The new Trump administration is shown in red. Results continue to be much better than Biden’s misery numbers. The advance is at a near minimum, given the Fed®’s policy.

Updated Civil War II Index

The Civil War II graphs are an attempt to measure four factors that might make Civil War II more likely, in real time. They are broken up into Violence, Political Instability, Economic Outlook, and Illegal Alien Crossings. As each of these is difficult to measure, I’ve created for three of the four metrics some leading indicators that combine to become the index. On illegal aliens, I’m just using government figures.

Violence:

Violence indicators are up slightly this month, and still elevated.

Political Instability:

Down is more stable, and it went down this month after the budget fight ended. I think the Somilisota scandal may increase pressures in a few months.

Economic:

The economy up just a smidge this month, but I think this is still cloaking the middle-class crunch and perhaps a bubble.

Illegal Aliens:

Still the lowest level since the Weather Report started.

LINKS

The links are again done by Ricky this month. Thanks, Ricky!

BAD GUYS

https://x.com/CaughtCam404/status/1998766070623252802

https://x.com/FoxNews/status/2006823362182394125

GOOD GUYS

https://x.com/StealthQE4/status/2006266481001001437

https://x.com/nickshirleyy/status/2004642794862961123

ONE GUY

https://abcnews.go.com/amp/US/oklahoma-man-target-practice-backyard-accused-fatally-shooting/story?id=128707327

https://realclearwire.com/articles/2025/12/13/wsjs_fearmongering_doesnt_survive_contact_with_evidence_153631.html

BODY COUNT

https://wir2026.wid.world/insight/executive-summary/

https://cms.zerohedge.com/s3/files/inline-images/All_the_Worlds_Births_Web-1.jpg?itok=z3Ci7zG4

https://www.nytimes.com/2025/12/28/business/us-immigration-trump-1920s.html?unlocked_article_code=1.AFA.WFF9.w9QS69D5L2fG&smid=url-share

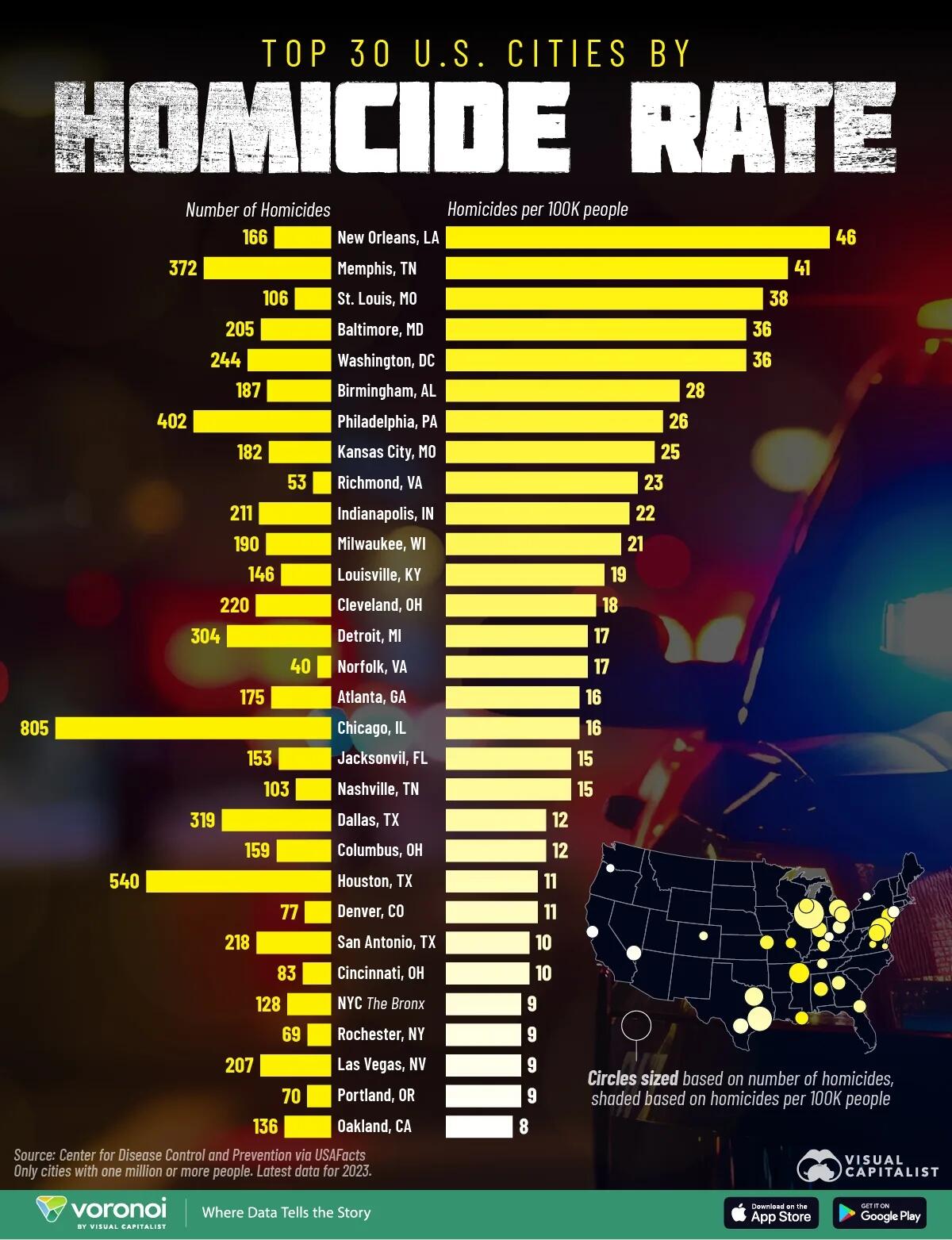

https://cms.zerohedge.com/s3/files/inline-images/Homicide_Rates_Web.jpg?itok=rn1aSBmf

https://studyfinds.org/churches-kept-americans-alive-states-made-a-decision/

https://www.thewrap.com/industry-news/business/entertainment-media-layoffs-2025-analysis/

https://www.theburningplatform.com/2025/12/19/dumber-sicker-poorer/

VOTE COUNT

https://thefederalist.com/2025/12/17/fulton-county-we-dont-dispute-315000-votes-lacking-poll-workers-signatures-were-counted-in-2020/

https://www.mediaite.com/politics/longtime-trump-pollster-reveals-ugly-forecast-for-republicans-heading-into-2026/

https://www.nbcnews.com/politics/2026-election/fight-young-men-2026-midterm-elections-rcna249513

https://www.cnn.com/politics/state-redistricting-maps-vis

CIVIL WAR

https://financialpreparedness.substack.com/p/who-are-the-bad-guys

https://brusselssignal.eu/2025/12/the-eu-could-be-gone-in-four-years-a-revolutionary-eruption-is-coming/

https://www.americanthinker.com/blog/2025/12/the_stages_of_a_color_revolution_and_where_the_u_s_is_right_now.html

https://rollcall.com/2025/10/08/civil-war-national-guard-midterm-elections/

https://www.civilbeat.org/2025/12/is-a-civil-war-possible-in-america-or-hawaii/

https://www.theburningplatform.com/2025/12/08/mass-collective-societal-suicide/

https://victorhanson.com/can-the-dark-ages-return/

“It’s a core meltdown, sir. It can’t be stopped.” – Galaxy Quest

Is your refrigerator running? If so, Ohioans may want to vote for it. (All memes as found in responses to Vivek’s tweets®)

As we slide into the end of 2025, Vivek Ramaswamy is at it again, melting down into a puddle on X™ like a little brown chocolate Easter rabbit in a sauna. Last year right around this time, Vivek was preaching that Americans are lazy sacks of mediocrity who need a flood of immigrants to save us from our own couch-potato culture.

In December 2024, Vivek dropped a bombshell thread on X®, blaming American culture for “venerating mediocrity over excellence” since (at least) the ‘90s, you know, when he was 10. Ramaswamy ranted about how we celebrate prom queens over math whizzes, jocks over valedictorians, and then made bizarre sitcom references.

His fix? Import more foreign-born people like, well, Vivek.

Because why?

Because, apparently, native Americans (not the feathered kind, the lazy you and me kind) can’t hack it. “Our American culture has venerated mediocrity over excellence for way too long,” he tweeted, as if the country that broke the sound barrier was built by sleepover parties and mall hangs.

The H-1Bs arrived starting in the 1990s. They didn’t build America. We didn’t need them to rescue us from squalor. They were an economic invasive species who flocked here because America was already great.

This year the blue monkey god he worships must have whispered in his ear, “It’s time, Vivek, make them hate you.”

Vivek is doubling down, insisting that no one is more American than anyone else. Blood doesn’t matter, loyalty to . . . I guess ‘90’s sitcoms . . . does.

The Wilder family tree is rooted deeper in American soil than a sequoia, so I’ll beg to differ. My ancestors have been buried in the United States for 250 years, fighting in every scrap from the Revolution to WWII.

Vivek? He’s a first-gen Hindu anchor baby whose parents, even today, aren’t American citizens. He really does worship a blue monkey god (Hanuman, for the uninitiated), I’m not making that up. Vivek, despite being tied to the United States neither by culture, blood, religion, or duration is lecturing us on what makes someone “American.”

This is irony thicker than his mother’s accent.

As I write this, Vivek’s second annual X® tantrum is in full swing. Running (currently losing) for Governor of Ohio, he’s gone into full defense mode. “Blood doesn’t make you American, loyalty does,” he posts, all while defending legal immigrants as often “the most American of us all.”

I’ll let you marinate on that one for a bit.

But here’s the rub: Vivek’s definition of Americanism is so broad it’s borderless. If it’s just about swearing allegiance and buying into “ideals” like consumerism and sacred cultural events like Toyotathon™, then every person on the planet is an American who just hasn’t hopped the fence yet.

Forget cultures that clash with ours, like those that prioritize caste (in his book, Vivek proudly notes he’s from the Brahmin caste) over equality, or Sharia over the Constitution.

Many immigrant cultures are absolutely antithetical to the American ethos the Founding Fathers baked in. Those guys weren’t dummies; they knew ancestry, culture, and religion were key to cohesion.

Jefferson warned about importing “principles adverse to freedom.”

Franklin fretted over Germans diluting the Anglo-Saxon stock, imagine what he’d think about Vivek.

They built a nation for “ourselves and our posterity,” not a global Airbnb® for anyone with a passport stamp. Vivek’s self-serving schtick reeks of opportunism. He’s a biotech billionaire who made his fortune through what looks an awful lot like pump and dump schemes. Remember Axovant™? His Roivant® spinoff hyped a failed Alzheimer’s drug that he bought for pennies, went public in a splashy IPO, and tanked when trials flopped.

This netted Vivek millions while investors ate dirt. Sounds familiar? It’s like Martin Shkreli’s pharma bro antics, but bigger and with better PR. Critics call it a “Wall Street speculator scam,” fleecing folks just like those Indian phone scammers who promise to fix your computer for a Playstation® gift cards.

Vivek’s version? Promise miracle drugs, pump the stock, dump before reality hits. Billions in the bank, ethics in the toilet, I mean, if he owns one.

And now he wants to govern Ohio?

Good luck selling that to Buckeye voters who value straight shooters over slick operators.

The irony is, Vivek’s behavior does more to stoke distrust of Indians than any redneck rant ever could. By shoving his “I’m as American as apple pie” narrative down our throats while ignoring cultural clashes, he alienates the very heartland he’s courting. Ohioans aren’t buying it.

Polls show the race tightening, but with AG Dave Yost calling the GOP endorsement of Vivek a “wrong choice,” and Democrats like Amy Acton gearing up, his path looks rockier than the Appalachians.

A Hindu lecturing Christians on American identity? In a state where churches outnumber tech startups?

He can’t win.

His meltdowns highlight the divide: America isn’t just ideals; it’s blood, soil, and shared history. Dilute that, and you get chaos.

What portends when this bubble bursts? Vivek’s campaign will fizzle like his drugs in trials. But the bigger fallout: his rhetoric erodes trust in assimilation. His little kids have Star Wars® names and worship a blue elephant god. I’ve said forever, if you didn’t consider naming your kid “Brandon” or “Jason” you’re clearly not American, and that takes roots that are about three generations deep.

If “loyalty” trumps culture, why stop at legal immigrants?

Why not amnesty everyone?

It’s a slippery slope to turning America into a mini-UN, where clashing values breed division. The Founders knew better: cohesion requires common roots.

Vivek’s vision? It’s a balkanizing civil war in the making.

In the end, meltdowns like Vivek’s are built on illusions: that America is just a proposition nation, no heritage required. But as my family’s graves attest, it’s more. He’s increasing dislike of Indians faster than a bad curry, all while scamming his way to the top.

Ohio deserves better. We’ve seen this show before (cough Obama cough) and know that electing someone who is clearly not American won’t make America better, but instead just leave little brown puddles everywhere.

“I had it all, even the glass dishes with tiny bubbles and imperfections.” – Fight Club

I wonder if Sean Connery is in 00 Heaven?

As we approach the end of 2025, the U.S. economy resembles a science-fair volcano built on baking soda, hype, construction paper, speculation, bubblegum, vinegar, and greed. I’ve written about this before, and, well, it’s so big it keeps dragging me back in.

The rot is birthed by several mothers: cheap cash, the need to put it somewhere, and a new technology whose benefits are (at this point) opaque at best. Let’s put down that you already know “money printer goes brrrrrrrr” so we’ll go back to A.I.

Again.

At the center of this precarious structure is what everyone who isn’t high on their own supply knows is an A.I. bubble. Large numbers of people (including me) recognized the housing bubble for what it was, but it kept on going because momentum is one hell of a master.

Another case of car-pole-tunnel syndrome.

A.I. has inflated stock prices, diverted resources like a drunk wine aunt at Lululemon®, and now has spawned secondary bubbles in hardware and infrastructure.

I’ve touched on this in previous posts, noting how projected AI:

But bubbles don’t exist in isolation. Bubbles multiply, feeding off each other until the inevitable pop unwinds it all. When the Great Housing Bubble burst, for example, sales of sulfuric acid went to zero for months. How are they related? Turns out the Great Housing Bubble was fed off the same credit structure that paid for basic chemicals.

And for all this time I thought it was because sulfuric acid was just like anything Chuck Schumer says: baseless and corrosive.

One time in chemistry they asked me to write 1,000 words on acid. I couldn’t finish it because my pen turned into a giraffe and the paper melted.

Today, we’re seeing this play out in real time, with AI-driven demand ripping into consumer electronics and beyond, all while broader market indicators flash warning signs of decline.

The AI stock bubble has birthed an investment bubble in virtually all computer hardware. Demand for specialized components has skyrocketed, pulling supply away from consumer markets and inflating prices across the board.

This shift isn’t just raising costs for gamers and everyday users; it’s distorting global supply chains, creating a feedback loop where AI hype justifies more investment, which in turn inflates hardware bubbles.

The statistics say cows kill more people than sharks, but I’m surprised that cows are killing any sharks.

What happens when the tide rolls out? With the underlying economy already showing recessionary cracks, the fallout will almost certainly be severe.

Let’s start with the AI bubble itself: valuations in the sector have soared, with companies like Nvidia™ and others commanding trillions in market cap based largely on future promises rather than current realities. The S&P 500’s concentration in a handful of AI-related stocks reached 30% by late 2025, the highest in decades. Nvidia© (for example) doubled in price from April.

Doubled.

Skepticism is now mounting.

All this is unfolding against a backdrop of broader economic weakness that A.I. papered over.

Oil prices are declining despite ongoing disruptions from wars in Ukraine and tensions with Iran. Price levels are back into COVID 2021 levels. This drop persists amid supply risks: Ukrainian drone strikes on Russian refineries and U.S. sanctions on Venezuelan tankers should theoretically support prices, yet oversupply fears dominate.

My dad once asked me, “Son, if you have a hot blonde rubbing oil on a hot brunette, what do you get?” I answered, “I don’t know, Pop.” “Your camera, son, your camera.” (as found)

If peace breaks out in Ukraine, bringing Russian oil fully back online, prices could plummet 30%-50% as sanctions lift and exports surge. Add in a resolution with Iran, and the glut could be historic—you might as well use oil for bubble baths. The IEA already forecasts surpluses building into 2026.

This is a signal of weakening industrial activity worldwide, not resilience.

Domestic indicators paint a similar picture. Unemployment among native-born Americans ticked up to 4.7% in July 2025 from 4.5% a year prior, with the overall rate holding at 4.6% in November.

Wages? They’re stagnant at best.

The K-shaped economy persists: high-wage earners see modest gains, but lower-income workers face stagnation, widening inequality.

So, what portends when the A.I. Bubble bursts?

History offers grim lessons: the Dotcom crash wiped out trillions and triggered a recession and the economic response to that caused he Great Recession. An A.I. pop could be worse, given its entanglement with hardware and infrastructure. It doesn’t help that it is spawned, in part, by the loose-money policies of the post-COVID world. If I’m making an SAT question, Dotcom is to The Great Recession as COVID is to ___________.

He then arrested me for assault with sandpaper. He didn’t accept the excuse that I’d only roughed the guy up a bit.

Consequences of it popping?

If this capital misallocation is as bad as some of the graphs I’ve seen, this will be the singular economic event of the lifetime of anyone alive. There is a reason that I picked 2032 as the central pivot point of when Civil War 2.0 would show up and it was the underlying financial mismanagement of the United States. A.I.? It’s not the gasoline in the room, it’s the spark.

It would have been something.

I made this and even though I replaced it with a more fitting meme up above, I figured you’d want to see it.

In the end, bubbles always burst because they’re built out of illusions and fed by poor allocations of capital. The A.I. frenzy has masked underlying frailties that would have led to a very major recession during Biden’s term, but the bubble continued to get bigger.

As oil slides, jobs stall, and hardware hype peaks, the reckoning looms. And that science-fair volcano? I hope I don’t drop it on my foot.

I’ll Krakatoa.

The usual. Not investment advice, do your own research, etc., etc.. I’m not a priest or an exorcist though I played one on TV. If you read this and make meaningful decisions based on it you need to take a step back and reconsider your life.

“The only good bug is a dead bug.” – Starship Troopers

Grok™ is getting better – this was a first attempt, and normally it requires a lot of wrestling.

OT: probably a Saturday song will drop tomorrow morning. I’ve got three more in can and think that two of the three are the best so far. I may even drop one on Sunday. We’ll see. Going forward I’m going to target dropping songs on Sunday, Tuesday, Thursday and Saturday. As I’ve just started, there seem to be an endless spring of ideas that I’ve been hoarding up my whole life, and I’m enjoying making them come to life. Oddly, I’m my new favorite artist. Working on distribution, still on a steep learning curve.

Once again, were’ back. The high of the 1980s is far in the rearview mirror. Now we’re on the long slope down. Still, there were some fun movies. These aren’t necessarily the best movies of 1997, instead they’re the films I think really exemplify the year. As always, they’re in no particular order.

Waiting for Guffman – This is an ensemble comedy where I think the plan was that you have a basic plot and you let the talented, goofy people making the movie fill in the details. Silly? Yes. Life changing? No. One thing from this particular movie that I find very sad is that the opening scene shows the local cops planning on having sniper overwatch for a local harvest festival in a small Missouri town. It was funny in 1997 because it was absurd. In 2025 it’s not. I guess that’s just the price we pay for ethic food. I wonder why we didn’t import only the recipes?

Austin Powers: International Man of Mystery – Mike Myers creates a parody of a James Bond® film. The particular genius is that the plot is just strong enough to hold everything together and not get in the way of the comedy. The box office was quadruple the cost, so that worked out okay for Mike. Bonus points for lovingly parodying the details of the Bond™ films, such as naming a female character Allota Fagina. Sadly, this caused the James Bond© producers to make the Bond® films less fun by hiring Daniel Craig.

Breakdown – There is nothing special about this movie other than it is a very competent thriller that couldn’t be made in the time of cell phones. Kurt Russell is good, and J.T. Walsh is suitably evil. Cinematic popcorn.

Men in Black – The X-Files™ was pretty big during this time period, so Hollywood decided to make a big budget science fiction comedy based on a fringe UFO topic. I was this many years old when I found out it was also based on a comic book. It made nearly $600 million 1997 bucks, which would have topped the box office for the year except for that pesky Titanic.

Contact – This was a decent movie, though not one where I look forward to seeing it again. It was decent, not great. Plot summary: aliens send us Hitler pics and instructions on how to build a wormhole.

Air Force One – More cinematic popcorn, where president Han Solo tries to kill Count Dracula on an airplane. Silly action fun.

Event Horizon – My favorite movie on this list. Huge critical and commercial failure and yet they nearly made a TV series based on it before COVID came along. Evil Scientist Sam Neill? Yes, please. If you like cosmic horror and haven’t seen it, you’ve been missing out. Warning: it’s not for the faint-hearted.

Kull the Conqueror – Robert E. Howard was the creator of Conan the Barbarian, and also Kull. This is based around his work, and was originally intended to be the third part of the Conan movie trilogy, but that fell apart. I’m glad. This movie is comfy and is its own thing. I loved it, and am perhaps the only one, since it only made $6 million on a $35 million budget. I guess I would suck as a test audience member.

L.A. Confidential – It came out in 1997, but I hadn’t seen it until recently. It’s a decent film noir, and Guy Pearce does a great job as a smart, young cop eager to get ahead. Huge hit, but I avoided it because I loathe Kim Basinger, who strikes me as a person with the intelligence of a basset hound.

Wishmaster – So an evil genie lives in a ruby. In one scene, the camera penetrates they gem, showing that it contains a vast cavern throne room inside the gem. In the cavern, it moves towards a dark, demonic figure sitting on the throne. During the scene, when the camera finally centered on the genie’s face, I said, “Just sitting ‘round, being evil,” and The Mrs. laughed uncontrollably. That’s now a family catchphrase. Other than that, I don’t remember anything about this movie.

Boogie Nights – This is a very good movie, showing how the depravity, drugs, and money of the porn world lead only to pain and dejection, but I’m sure OnlyFans® will turn out differently. Plus? Stark nekkid Heather Graham. Okay, I have contradictory motivations here. Also, one of Burt Reynolds’ best serious roles.

RocketMan – Cost $16 million to make, made $15.4 million. It was hilarious. The underappreciated Harland Williams plays an accidental astronaut whose space hijinks include space farts. It’s stupid-funny, so if you like adolescent humor, this is your show.

Bean – Rowan Atkinson is an engineer with a master’s degree and also a master of comedy. Who says engineers don’t have a sense of humor? Oh, and this film made $250,000,000.

The Devil’s Advocate – Soooooo much overacting in this horror movie which could have also been titled “Al Pacino’s Vocal Coach Is Seventeen Packs of Cigarettes a Day.” No real desire to watch this one again – it’s not a great horror movie, but everyone liked it, because the boxoffice of $153,000,000 was nearly triple the cost.

Gattaca – This movie is about the dangers of genetic engineering on the future, where it creates a society where beautiful, healthy people are everywhere and bad genes are bred out. The horror!

Starship Troopers – Whenever this movie comes up in the comment section everyone argues about it. Every time. Was director Paul Verhoeven trying to make Robert Heinlein look like a fascist and make the humans as the bad guys? Yes. Did almost everyone miss that? Also yes. To try to make fun of Heinlein, he had to actually quote Heinlein, which backfired in a big way. Heinlein’s ideas in the book Starship Troopers are pretty powerful, but also simple. They glimmered through Verhoeven’s attempt to make a woke film, which counts for most of the good parts of the film. But the other fascist elements he added for the parody boomeranged on him to such an extent that all of the GloboLeft critics he wanted to please by making fun of the TradRight thought Verhoeven was a fascist. I guess he sure showed the TradRight by being pro-human rather than loving bugs. My verdict? The only good things (which are very good) are the parts from the book. The rest is mediocre at best.

Once again, I was surprised on how many movies I liked from this year. Almost every movie is beautiful, but the attempts are being made to push the GloboLeft agenda even further, which is (along with foreign markets) what eventually choked Hollywood. I’m debating if we’ll do 1998, and if so, that’ll be in February.

What did I miss?

“I have become death, destroyer of worlds.” – Andromeda

Had Oppenheimer been a theoretical physicist he would have been frictionless, perfectly spherical, homogeneous, isotropic, involuntarily celibate, and have extended to infinity in all directions. I guess one out of seven isn’t bad.

You know, Oppenheimer probably didn’t realize that his little gadget would one day power cat videos on YouTube®. But yet, here we are, preparing to stare down the barrel of an energy crisis that makes the 1970s oil embargo look like a minor hiccup at the gas pump.

America’s tech overlords are building A.I. data centers faster than a caffeinated beaver on gas station Chinese boner pills. These behemoths suck down electricity like it’s free beer at an open bar to toss electrons so we can make A.I. cat videos because there weren’t enough cats in real life.

The scale is enormous: gigawatts upon gigawatts, enough to finally get Marty all the way back to 1985. But that begs this question:

Where’s all that juice coming from?

My walkie-talkie once took a lump of coal to a movie. It was a classic example of radio-carbon dating.

Coal? Ha! That’s so 19th century, and the eco-warriors have pretty much chained themselves to the last coal plant, screaming about carbon footprints.

Natural gas? Did everyone forget demand peaks in winter when everyone is cranking up the heat and prices spike like Nvidia® stock? Are we going to have to keep our homes at 40°F (3.14 millipedes) just so ChatGPT® can make GloboLeftist women on the East Coast even more neurotic?

We need power, so, naturally, the bright sparks in Silicon Valley and D.C. turn to the holy grail: The Simpsons.

Sure, Homer® looks incompetent, but he hasn’t melted Springfield down. Yet. When The Simpsons started, they were mocking nuclear power in the typical GloboLeft drive to get it shut down.

Deep down, though, nuclear really always has been the only viable transition plan into the future. Oil really will run out at some point, abiotic or not.

I had an allergic reaction and the doctor asked how I was. “Swell.”

But nuclear? If done right, it really can be clean, reliable, and if we don’t let Soviets do it, pretty safe.

So, problem solved.

Not.

We’re facing an immediate energy cliff. In 2025, nuclear isn’t a parachute, it’s really more like a bedsheet and some twine.

With a little help from Constant Reader Ricky, who sent me an email.

I’ll quote him directly because, well, he nails it better than I could.

Ricky writes: “Existing commercial power reactors in the US have two key characteristics – their uranium is enriched from the natural 0.7% U-235 assay to a level of 3%, and they are cooled with pressurized water as the heat transfer fluid to run the turbines. The reactors were INITIALLY fueled via uranium enrichment done long ago in . . . monstrous factories that are now closed. An effectively experimental centrifuge enrichment operation in Piketon, Ohio shut down in 2016 without ever producing a pound of reactor fuel (we bombed a similar setup recently in Iran).

“Believe it or not, the US CURRENTLY fuels its commercial nuclear power reactors for the past ten years with Russian 3% enriched uranium, even through the Ukrainian war. The Russians basically dilute some of their bomb grade 93% enriched uranium stockpile down into 3% reactor fuel as an export profit center.”

Key point courtesy of Ricky: “The current American commercial nuclear power program is 100% dependent on the Russians and has been for the last decade.” He adds, “But we want that because that every kilogram of Russian uranium that goes IN a New York City power reactor is one less kilogram of Russian uranium that can go into an incoming nuclear bomb OVER New York City.”

He’s right. I want the Russians to hit the Somilsotans first. And then New York City twice. It’s the only way to be sure.

And just like uranium, Hillary is unstable, hard to find, and expensive. If only we could power a reactor with her tears.

It’s like we’re in a bad spy novel, relying on our geopolitical rivals for the fuel that keeps our lights on. We can stamp our feet as much as we want to, but as long as Mom and Dad are paying the power bills, they call the shots.

With AI data centers projected to gobble up an extra 200-300 gigawatts by 2050 (that’s tripling our nuclear capacity), we’re supposed to ramp up nuclear like it’s no big deal. It’s like the steady high school girlfriend you’ve been dating off and on for a year who you can always call for a date at the last minute.

Nope.

Building that kind of capacity?

Recent estimates peg adding just 63 GW at $354 billion. We’re talking trillions when you factor in overruns. The Vogtle plant in Georgia – two reactors, “just” 2.2 GW, clocked in at $35 billion after fifteen years of delays.

Nuclear power makes NASA look prompt and frugal.

Okay, we’ll just do micro-reactors.

Except these micro wonders ditch the “obsolete” 3% enriched uranium for something hotter: 20% enriched stuff, packaged in pellets like, I don’t know, energy kibble. Supposedly, they’re meltdown-proof, corrosion-resistant, great with kids, fun at parties, and perfect for high-temperature gas or molten salt reactors. And they’re much smaller than kibble, like poppy seed sized, but kibble is a funnier word and I really don’t want to think how stupid it is to build highly radioactive balls that you could put into someone’s potato salad at the neighborhood picnic?

I did figure out where I got the plague: the flea market.

Cool, so where do we get this 20% enriched uranium for our nuclear kibble?

We downblend our surplus bomb-grade stuff from the Cold War.

The US has 480 metric tons total, but half is reserved for nuking India (it’s the only way to be sure), and 100 tons reserved for Navy reactors.

Bringing those numbers up to date and turning it into nuclear kibble leaves 86 metric tons up for grabs.

So, we have a safe plan. What’s stopping us?

Adding 250 GW of new nuclear by 2050 (a Department of Energy guess) requires 5,350 metric tons (it’s like a ton, but it has a French accent) of enriched uranium kibble.

Do the math:

86 tons available vs. 5,350 needed?

It’s like trying to fill an Olympic®-sized pool by spitting into it.

Our energy policy in a single meme.

Okay, let’s restart a program that used to make the stuff. Great! The Piketon, Ohio centrifuge plant we mentioned above, let’s use that. They’re planning on delivering 900 kilograms (a ton for those of us from countries that have put people on the Moon) by 2026.

So, we need over 5,000 tons.

We’ve made one. Oh, scratch that, not even one yet.

Want to take odds on that bet?

Even if we magically create tons of usable uranium, Harry Potter-style®, there’s no supply chain for turning it into nuclear kibble. Right now, it’s a prototype lab in New Mexico fiddling with demos.

We’d need a whole new industry.

And we’d need to have started on this (checks watch) twenty years ago. That’s the bitch of exponential growth. We could play with 2030 numbers (“only” 50 GW), but since no concrete has been poured for this new capacity and there is no path to creating this fuel, it’s more realistic to discuss if Superman© could beat The Witcher®. It’s a non-starter.

I mean, who would win, Captain Kirk or T.J. Hooker?

We’re dependent on foreign fuel, short on domestic capacity, and staring at timelines measured in decades, not quarters.

Maybe it’s time to rethink the whole “AI will save us” stock market hype or at least stock up on candles and spears.

And hey, if that microreactor ends up in my yard, Homer© and I will host a barbecue, BYOGC.

(Bring your own Geiger counters, you know, potato salad).

Thank heavens we let The Simpsons create our energy policy.

“How do you hunt a bear in winter? Go in his cave with spears.” – The 13th Warrior

I bought some spears on E-Bay® but when they arrived, they were all missing their points. I guess I got shafted. (all art is A.I. generated)

Ahhh, innovation, that Pandora’s Box that has poppled up again and again in the Self-Stor® of history in the back corner underneath the stack of old National Geographics®: “Why do it the hard way when you can do it the smart way?”

In paleolithic times, the technology was napped stone turned into a spear point. Oh, sure, the old folks said, “We didn’t need any of those fancy flint spears when I was growing, up, we just took down the mammoth with our fingernails and teeth,” but the overall access to calories for the tribe, one measure of their wealth (along with number of remaining teeth), increased.

This was doing things in a more indirect manner and is one of the oldest examples we have of human-like behavior in the archeological record. Rather than try to gnaw a mammoth to death, the idea was to spend time finding and crafting a piece of wood into a shaft, knapping a stone spearpoint, using a leather thong and wrapping the whole thing up to make an easier way to take down a mammoth than just using incisors.

I don’t see much of a downside to this technology (I mean, besides the whole war thing that came with it), and it certainly scaled quickly.

I saw a mammoth singing Calypso. His name was Hairy Elephante.

Other examples include:

Technology is that replacement of some aspect of our life that is difficult with one that is much more indirect, yet makes the task easier. These changes fundamentally changed society.

The Agricultural Revolution was one, turning humanity from wandering bands of dudes who spent all day in the outdoors hunting to dudes that could now have 9 to 5 jobs and backaches from plowing. Oh, and taxes. Yup, taxes and mortgages and debt.

Ouch.

The Mrs. told me she was getting tired of the corny jokes. So, I decided to do jokes about chemistry, but was worried about the reaction.

The Industrial Revolution was another, turning humanity from relying on animal and human effort into one where chemical release of energy made slavery uneconomical, also creating the first case of obsolete farm equipment. The economics of the Industrial Revolution led to the end of slavery in the West (there are more slaves in Africa right now than there were in the United States before the Civil War), not ethics or virtue signaling.

But this controlled chemical release of energy made so many other changes possible. Energy had been very expensive, and now it was, by historical standards, cheap. Many innovations followed in rapid succession because of this singular change. Trains, telegraphs, textiles, tapioca, trampolines, toilets, televisions and PEZ® can all trace their existence or mass production back to the Industrial Revolution. Oh, and child labor.

What’s short, tired, and very profitable? Child labor.

Let’s look at one consequence of the Industrial Revolution:

In order for people on the coasts to have fresh meat, railroads had to move live cattle from the center of the United States to the coasts. This required watering and feeding along the way, and was expensive since lots of cattle parts that people didn’t want to eat (like hooves and heads and hair and hides and other parts starting with the letter “H”) had to be moved as well. It was expensive to move what was to a butcher in New York City, nothing more than waste to discard.

The innovation of a refrigerated rail car changed all of that: cattle could be slaughtered all in one location, and everything from them could be used in subsequent products, bones for glues and buttons, hides for leather dominatrix boots, leather for dominatrix whips, and, well, you get the idea. This is where the famous quote on pork production by Upton Sinclair came from, “ . . . use everything but the squeal.”

It also changed and allowed monopolization of the market. Now, due to the organization of massive slaughterhouses and meat production facilities, ancillary factories like tanneries and sausage plants and glue factories could also be built, which explains Chicago.

Almost all multiple stabbings are committed by someone very close to the victim. Arm’s length, at most.

Chicago became the terminus for cattle heading nationwide. This gave the buyer huge amounts of influence, since now purchasing of cattle became centralized, the purchasers could set their price. Likewise, the cost structure changed to the point where producers could nearly give the meat away for free due to the profits from the rest of the animal.

This concentration of power allowed the profits to be centralized, and with only two or three players, they colluded to make as much money as they wanted. This did increase the overall wealth since now people in New York could get decent steaks. Also, I suppose people wanted those slaughterhouse jobs or else Upton Sinclair’s book, The Jungle, wouldn’t have been such a powerful recruiting tool.

It did provide just one example of a technology that was greatly disruptive, and changed an industry, centralizing it, and making the extraction of profits at a single point possible. Congressional action in the form of the Packers and Stockyards Act of 1921 was necessary to break up the five-company oligopoly.

I once read about a motor that was too powerful for the moving stairway – it escalated very quickly.

Weird how we recognized the danger of capital concentration back then instead of providing infinity bailouts. We recognized that technology should work for us, and feared the concentrated power of both government and corporations.

Now? We have a domination of the economy in a similar fashion, for similar reasons: the Internet made information access trivial, leading to the collapse of the existing commerce and distribution system. Oh, yeah, it’s the gateway to the technology that is already disrupting the economy on a scale that meat packing never could:

Intelligence.

Okay, not exactly intelligence. But in certain applications it can do wonders. I had a phone call with my credit card company. The call was crisp, clear, relevant and in perfect English. Only when I asked a non-standard question did the odd hesitations and gaps show up, and it transferred me to . . . “Peggy” whose thick Hyderabad accent told me her name wasn’t really Peggy. Peggy was able to answer my final question.

How many lawyers does it take to change a lightbulb? Don’t know, the jury is still out.

A.I. has taken over a conversation and now some Indian was out 7.5 rupees, or whatever the name is of that colored wrapping paper they use for a currency is.

This is just the beginning. I had an A.I. tech support question where the answer came in a chat window – three or four messages, one last “Did you try this?” and the problem was fixed.

Heart surgery soon? No. Controlling telemedicine and serving up patients to doctors who have been prepped by an A.I. assistant?

Yes. And artists? They’re now competing against free.

I hate making spelling mistakes on this blog. Just one and the whole post is urined. (in fairness to Grok®, it got the spelling correct on one of the two)

And control of A.I. is all concentrated in server farms and Seattle silos. If 11.7% of jobs in the United States are, as a recent MIT estimate showed, in danger of A.I. replacement.

But add on the indirect jobs lost, you know, because 11.7% of jobs that pay decent wages go away? The numbers show that the job losses that follow because that 11.7% aren’t going to McDonald’s® anymore could jump to a combined 27.4% drop in unemployment, a Great Depression level number.

This is a calculation, not a blind guess. In technical terms, that means it’s still wrong, but I’ll be able to explain why. Using Okun’s “Law” (about 2% GDP drop from each 1% unemployment rise) that calculates to a 50%+ drop in GDP.

Nah, it’ll be fine.

We still know how to make spears.

{kind=link}

{kind=link}